Millions upon millions of Americans lost their jobs in March 2020, when the United States began its meager fight against COVID-19. Though a financial aid package from the Federal Government helped to mitigate the mass unemployment with stimulus checks and boosted unemployment payments, many people are continuing to suffer financial hardship as a result of the crisis.

Whether you have just managed to regain employment after COVID-19 or you have obtained your first job ever, you need to make smart choices with your money to secure financial stability into the future. Here are some strong suggestions for money management to make the most of your current employment status:

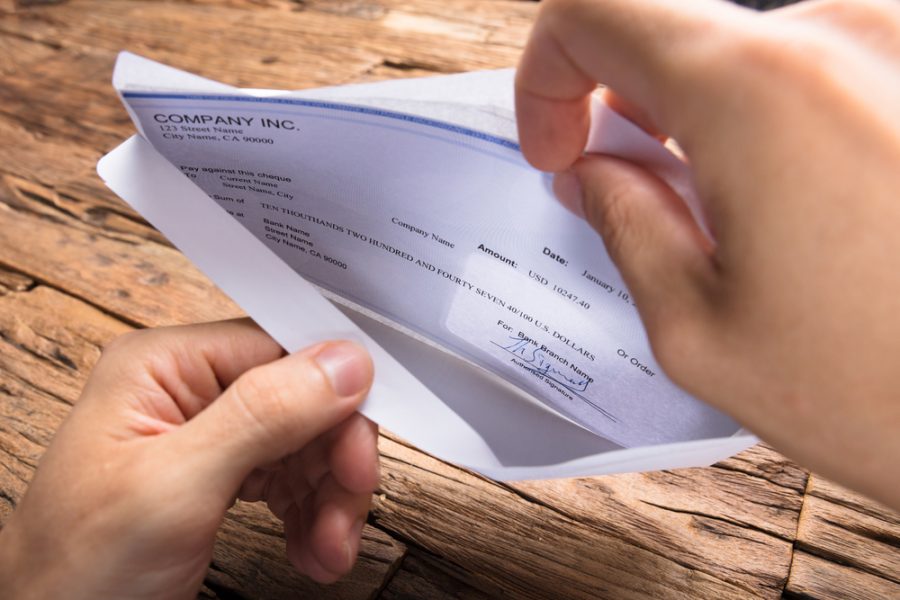

Direct Deposit Your Paycheck

Almost all employers in 2020 offer the option of free direct deposit into a bank account, and you should take advantage of this perk as soon as you can. Not only is direct deposit convenient, ensuring that you are paid on time and (usually) in full without the hassle of visiting the bank or the opportunity to lose your check, but it also means you have less temptation to cash and spend your entire paycheck at once (or worse, visit a payday loan provider). It is a small action, but it is one that can impact your financial habits down the line.

Automate Your Savings Contributions

You need at least two different types of savings accounts for enhanced financial stability: retirement and emergency. Your new employer might offer retirement savings options, like a 401(k) or IRA, and they might also match your contributes to your retirement fund by a certain percentage or to a certain limit. You should talk to HR about your in-house retirement savings opportunities. If your employer does not offer any retirement options (an increasingly common occurrence) you might talk to a financial advisor at your financial institution or else research IRAs online. How much money you put into retirement will depend on your income and expenses now and into the future.

Your employer will not offer help in building an emergency savings fund, and that makes it even more important that you devote time and resources to compiling your own. Your emergency savings should have enough money to pay for between three and six months’ worth of expenses, should you suddenly and unexpectedly lose your income. You shouldn’t dip into emergency savings for any whim; this money should be reserved for only the direst circumstances.

For both retirement and emergency savings — as well as any other savings goals you might have — you should consider automating your contributions. Most financial institutions allow you to set up automatic deposits into savings accounts from your checking. By automating the process of saving, you again eliminate the temptation to spend all your hard-earned cash and you ensure that your most important savings goals are met.

Build a Better Budget

Now that you have the income from employment, you can alter your existing budget or build a new one from scratch. Your budget should help you with money management, ensuring that you have enough cash to pay for living essentials (rent, utilities, food, etc.) and achieve your financial goals (retirement, emergency savings, travel savings, etc.) while enjoying your new income and upgrading your lifestyle. There are many budget templates you can find online, but it is important to remember that tinkering with spreadsheets is less important than living your budget every day — avoiding spending too much on certain things and focusing on building your wealth over time.

Reward Yourself (Sometimes)

Proper money management shouldn’t be an interminable slog. You work for your money, and you should feel allowed to use your money to make yourself happy. Your budget should give you the space to spend on activities or items that bring you joy, like a trip to the movies or a new dress. You might also give yourself quarterly or biannual rewards — larger purchases that improve your lifestyle or attitude considerably, like new furniture or a short trip. You won’t be able to build financial stability and wealth if you devote all of your income to rewards, but you won’t be able to commit to your financial plan if you don’t give yourself wiggle room to have fun.

Now that you have a job, you have more financial responsibilities. You need to spend enough on your lifestyle to ensure that you can keep your job, and you need to contribute to your future with strategic saving. By developing a financial plan, you can feel more secure and truly enjoy your newfound employment.